Key Takeaways

- Your most important decade for CPF is your 30s — SA contributions compounding at 4% for 20+ years create the largest retirement balance gains of any period

- If you are in your 30s and have not started SA top-ups, you may be leaving $50,000+ in compound interest on the table by waiting another decade

- In your 40s, maximise the $8,000 annual SA top-up tax relief — you have the income to do it and enough time left for it to matter significantly

- In your 50s, the pre-55 window for SA top-ups closes permanently — every year you delay is a year of 4% compounding that cannot be recovered

- The OA-to-SA transfer is irreversible and must be considered carefully at every age

The Life Timeline: Where You Are Changes Everything

Age 25–35: Foundation Phase └─ Build OA for housing | Let SA compound quietly | Learn the system Age 35–45: Growth Phase └─ Start SA top-ups aggressively | Claim $8,000 tax relief | Check FRS trajectory Age 45–55: Acceleration Phase └─ Max RSTU every year | Close the FRS gap | Final SA push before 55 Age 55+: Distribution Phase └─ RA compounds at 4% | Manage CPF LIFE options | Consider deferring payouts

Summary Table: CPF Priorities by Decade

| Age Group | Primary Focus | Why It Matters |

|---|---|---|

| 20s | Understand the system; build OA; let SA compound | Foundation for both housing and retirement |

| 30s | Start voluntary SA top-ups; check FRS trajectory | The time advantage of 4% compounding is largest here |

| 40s | Maximise $8,000 SA top-up annually; check property position | High income + meaningful time horizon = maximum efficiency |

| 50s | Final SA top-ups before 55; understand RA formation; plan property moves | The window closes at 55; decisions made here are permanent |

In Your 20s: Build the Foundation

Your under-35 CPF allocation puts 23% of your salary into OA — the highest OA allocation of any age group. SA receives 6% and MA receives 8%. Your SA balance is growing quietly at 4% p.a. The compounding clock has started, and it is the most valuable clock in your financial life.

What to Do

Learn the system first. Understanding the OW ceiling, account allocations, and the purpose of each account is more valuable than any single financial decision in your 20s.

Do not rush property. The temptation to use OA for a flat purchase is understandable, but early property purchases lock up OA funds and create an accrued interest obligation. Every year you wait before buying is another year of OA compounding at 2.5% with no accrued interest clock running.

Avoid the OA-to-SA transfer unless your housing plans are clear. At 25, the transfer looks mathematically attractive — you move from 2.5% to 4%. But if you need OA for a flat in your late 20s or early 30s, the irreversibility becomes a problem.

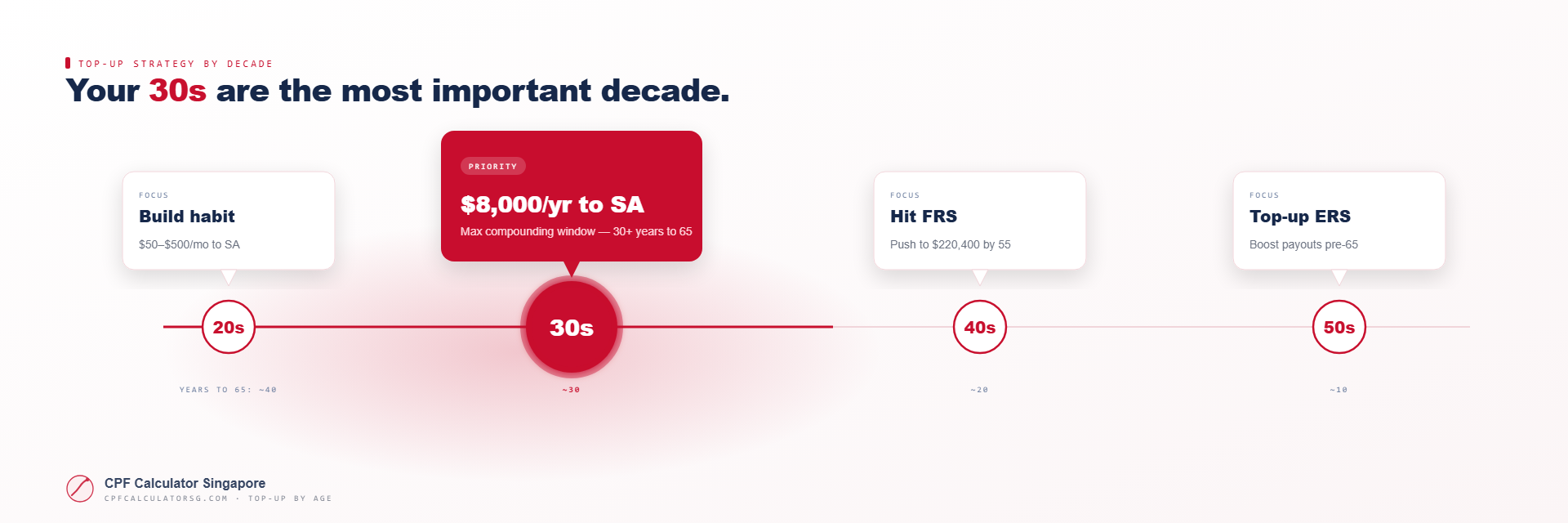

In Your 30s: The Most Important Decade

This is the point where the mathematics become stark and cannot be ignored.

At 35, your SA has 20 years to compound before you turn 55. At 4% p.a., $50,000 in SA at age 35 becomes approximately $110,000 by 55 with no additional contributions. The same $50,000 contributed at age 45 grows to only $74,000. The 10-year delay costs you $36,000 on a single $50,000 contribution. It cannot be recovered.

A 30s Checkpoint: Are You on Track?

| SA Balance at 35 | Projected SA at 55 (4% p.a., no top-ups) | Gap to FRS ~$330,000 |

|---|---|---|

| $30,000 | ~$66,000 | Large gap — top-ups are essential |

| $60,000 | ~$131,000 | Meaningful gap — top-ups are important |

| $100,000 | ~$219,000 | Manageable gap — top-ups still useful |

What to Do

- Start voluntary SA cash top-ups. Even $2,000–$3,000/year is worth doing. Starting the habit now is far more important than starting perfectly later.

- Claim the tax relief every year. Every cash top-up to SA (up to $8,000/year) reduces your taxable income.

- Check your FRS trajectory. The FRS for 2026 is $220,400. By 2041, the FRS will be approximately $330,000–$350,000. Your SA balance at 50 should be within striking distance.

In Your 40s: Maximise the Efficiency Window

By your 40s, you are likely earning more than in your 30s. The $8,000 SA top-up costs you less in relative terms. And you still have 10–15 years before 55 — enough time for meaningful compounding.

At the same time, the cost of inaction rises sharply. A $10,000 SA contribution at 45 grows to approximately $21,900 by 65 (4% p.a. for 20 years). The same $10,000 contributed at 50 grows to only $17,900 by 65. Every year of delay has a measurable, permanent cost.

What to Do

- Make the $8,000 annual SA top-up a standing commitment. At a 15–18% marginal tax rate, the effective cost after tax relief is $6,720–$6,560. Set it up as a recurring reminder in December each year.

- Top up family members' SA/RA as well. If your parents have CPF accounts, a top-up to their RA gives them higher CPF LIFE payouts and gives you additional tax relief (up to $8,000 family combined).

- Run a retirement gap calculation. By 45, you have enough data to project your SA balance at 55 and your gap to FRS. Use the CPF Calculator to model this.

Model your SA balance trajectory and see where targeted top-ups have the greatest impact.

Run Your CPF Projection →In Your 50s: The Final Push Before 55 Changes Everything

What Happens at 55

- A Retirement Account (RA) is created

- SA balances are swept into RA up to the prevailing FRS of $220,400

- Your SA is closed as a top-up destination — from 55 onwards, voluntary cash top-ups go to RA instead

- You become eligible to withdraw CPF savings above the FRS (or BRS if you have a property pledge)

The pre-55 period is the only window for SA contributions. Once it closes, it closes permanently.

Pre-55 Countdown Checklist

- Calculate current SA balance and gap to FRS ($220,400 in 2026 terms)

- Commit to annual $8,000 cash top-ups every year until you turn 55

- Consider an OA-to-SA transfer if OA balance is large and housing is settled

- Review all CPF nominations — ensure they are current

- Model your CPF LIFE payout at current projected RA balance via my.cpf.gov.sg

- Check accrued interest on any property where CPF was used

The Long View: Compound Interest as a Strategy

| Age When Contribution Made | Amount | Value at 65 (4% p.a.) |

|---|---|---|

| 30 | $10,000 | ~$43,000 |

| 35 | $10,000 | ~$35,000 |

| 40 | $10,000 | ~$29,000 |

| 45 | $10,000 | ~$24,000 |

| 50 | $10,000 | ~$20,000 |

| 54 | $10,000 | ~$16,000 |

The same $10,000 at 30 is worth 2.7 times more at 65 than the same $10,000 at 54. Time is not just helpful — it is the primary variable. The compound interest machine is already running. The question is whether you are feeding it.

Frequently Asked Questions

I am 42 and have never made a voluntary SA top-up. Is it too late?

It is not too late — but the urgency is real. You have 13 years before your 55th birthday. An $8,000/year voluntary top-up starting now, compounding at 4%, would add approximately $110,000 to your SA by 55. That meaningfully changes your CPF LIFE payout from 65.

Should I do the OA-to-SA transfer or a cash top-up?

These are separate decisions. An OA-to-SA transfer moves existing CPF money from 2.5% to 4% — no tax relief, but a guaranteed 1.5% rate improvement. A cash top-up via RSTU brings new money into SA and delivers up to $8,000/year in income tax relief. If you have cash available and your OA is needed for housing, do the cash top-up first.

If I top up SA in my 30s, does it affect my ability to use CPF for housing?

No — SA top-ups do not touch your OA. Housing purchases and mortgage repayments come from OA only. Topping up SA leaves your OA completely untouched.

What if I start topping up late — say at 50 — is it still worth it?

Yes. At 50, you have 5 years before SA closes at 55. An $8,000/year top-up over 5 years at 4% adds approximately $43,000 to your SA by 55 — and reduces your tax bill by $6,000–$14,000 over that period.

Can I use SRS instead of CPF top-ups?

CPF should generally come first. SA/RA earns a guaranteed 4% with no market risk; SRS depends on your investment choices. CPF LIFE is also a lifelong annuity, which SRS is not. See CPF vs SRS: Where Should You Put Your Retirement Money? for a full comparison.

Written by the team at CPF Calculator SG. Reviewed against CPF Board policies effective January 2026. For the authoritative source, visit cpf.gov.sg. This article is for general information only and does not constitute financial advice.