Last reviewed: May 2026 | Next review: January 2027 | Reading time: 8 min

Key Takeaways

- Self-employed CPF: MediSave is mandatory (if NTI > $6,000/year), OA and SA are voluntary

- MediSave contribution: ~10% of Net Trade Income, capped at ~$8,880/year

- Most freelancers discover this at tax time — 12–18 months after going solo

- Voluntary SA top-ups earn 4% guaranteed + qualify for $8,000/year tax relief

- Without voluntary contributions, your CPF LIFE payout at 65 could be zero

Nobody told you this when you went freelance.

When you left your salaried job, your CPF contributions dropped to zero. No employer, no mandatory deductions, more cash in hand. It felt like a raise.

But here's what the CPF booklet doesn't make obvious: as a self-employed person, you still owe CPF. Just not the part you're thinking of.

Every self-employed Singaporean with Net Trade Income above $6,000/year must make annual MediSave contributions. And many freelancers only discover this when they file their taxes for the first time — and get hit with a bill they weren't expecting.

This article explains what you owe, what you don't, and why voluntarily putting money into CPF is one of the best financial moves a freelancer can make.

The Core Rule: What's Mandatory for Self-Employed

| Account | Mandatory? | Notes |

|---|---|---|

| MediSave (MA) | Yes — if NTI ≥ $6,001 | Assessed annually when you file income tax |

| Ordinary Account (OA) | No | Voluntary only |

| Special Account (SA) | No | Voluntary only |

This is the key difference from employment: there is no employer paying CPF on your behalf. You are the employer. And as the employer, you've essentially opted out of OA and SA by choosing self-employment — but the MediSave obligation follows you regardless.

The MediSave Contribution Table for Self-Employed

MediSave contributions are calculated on your Net Trade Income (NTI) — your gross business revenue minus allowable business expenses, before personal income tax deductions.

| Net Trade Income (NTI) | Approximate Contribution |

|---|---|

| Below $6,000 | No contribution required |

| $6,000 – $12,000 | ~4% of NTI |

| $12,000 – $18,000 | ~4.5% of NTI |

| $18,000 – $24,000 | ~5% of NTI |

| $24,000 – $30,000 | ~5.5% of NTI |

| $30,000 – $60,000 | ~8–9% of NTI |

| $60,000 and above | ~10% of NTI |

Capped at the MediSave Annual Contribution Ceiling: approximately $8,880/year (2026).

There is also an account cap: once your MediSave account reaches the Basic Healthcare Sum (BHS): $75,500 (2026), mandatory contributions stop. If your MA is already at the BHS, you owe nothing — even with high NTI.

Calculate your exact CPF contributions based on your salary, age and citizenship status.

Open the Free CPF Calculator →Uncle Lim's Real Numbers

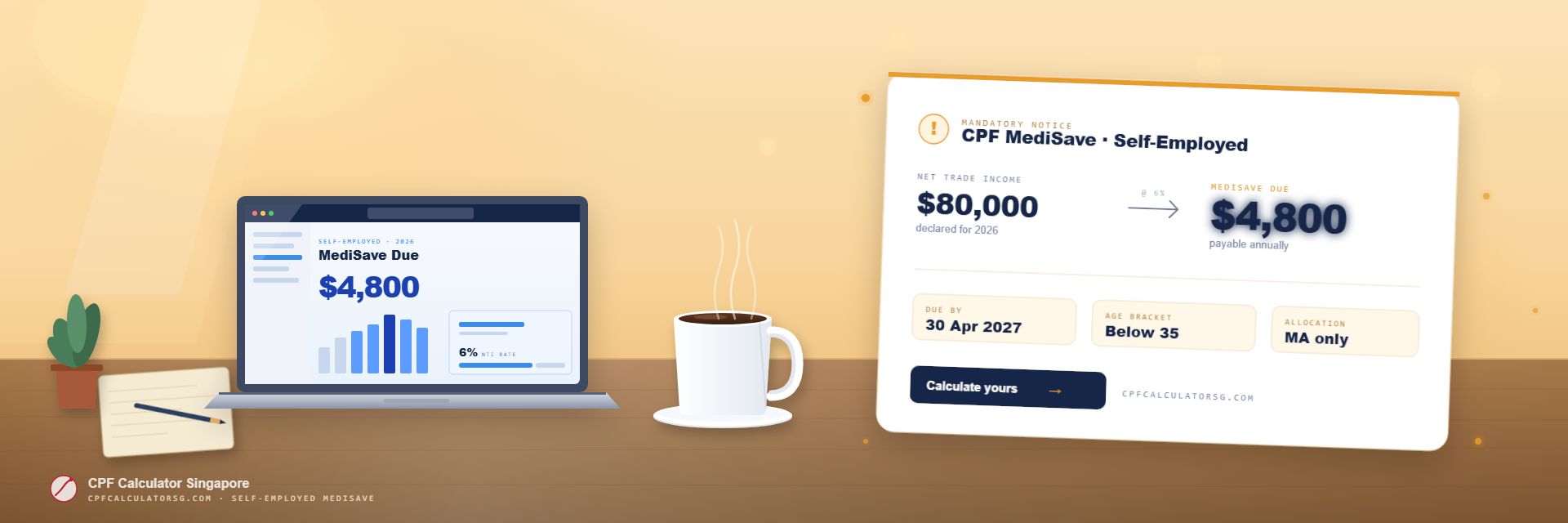

Uncle Lim runs an IT consultancy. NTI this year: $80,000.

Mandatory MediSave contribution:

At $80,000 NTI, the contribution rate is approximately 10% of NTI, subject to the annual cap of $8,880.

Estimated mandatory MediSave contribution: $8,000/year (10% of $80,000, capped at $8,880).

This is paid once per year, assessed after Uncle Lim files his income tax. IRAS and CPF Board communicate automatically — Uncle Lim gets notified of his MediSave obligation during tax season (typically June/July).

If Uncle Lim forgets to budget for this: he'll face a payment demand in June/July that catches most first-year freelancers cold. Plan for it.

⚠️ Important: The Freelancer's Tax-Season Surprise

Many freelancers only discover their MediSave obligation when they receive their tax assessment — often 12–18 months after their first year of self-employment.

By then:

- They've spent the "extra cash" from not having CPF deducted

- They face a lump-sum MediSave payment demand

- For high earners, this can be $6,000–$8,880 or more due in a single paymentWhat to do: From your first month of self-employment, set aside 10% of your monthly invoicing into a separate account. Use it to pay your MediSave assessment. Anything left over is genuinely yours.

Why Voluntary Contributions Still Make Sense

Just because OA and SA are optional doesn't mean they're a bad idea.

Here's what voluntary CPF contributions give Uncle Lim:

1. Compounding at 4%

SA earns 4% guaranteed. No stock market risk. No currency exposure. No management fee. For a freelancer who wants a reliable baseline retirement fund, this is hard to beat.

2. Tax Deductions

Cash top-ups to SA/RA and MA are tax-deductible under the RSTU scheme:

- Top up your own SA/RA: up to $8,000/year in tax relief

- Top up a family member's SA/RA: additional $8,000/year in tax relief

Uncle Lim's NTI: $80,000. Marginal tax rate at that level: approximately 11.5%. If he tops up $8,000 to SA, he saves ~$920 in tax and the $8,000 earns 4% in SA. Effective yield factoring in tax savings is well above 4%.

3. CPF LIFE Eligibility

CPF LIFE payouts require a minimum RA balance at age 65. Freelancers who only make mandatory MediSave contributions may have very little in OA/SA and therefore a very small RA at 55 — leading to minimal or zero CPF LIFE payouts.

Voluntarily building SA throughout your freelance career is the fix.

The Retirement Gap: Two Versions of Uncle Lim at 65

Let's project two scenarios for Uncle Lim (now 40, NTI $80,000/year through to 65):

Version A: Only mandatory MediSave contributions

- OA: $0 accumulated (no voluntary contributions)

- SA: $0 accumulated

- MA: Maxes out at BHS ($75,500) around age 48 given $8K/year contributions

- RA at 55: minimal (SA was empty, OA was empty — nothing to sweep into RA)

- CPF LIFE payout at 65: minimal or zero

Version B: Mandatory MediSave + $500/month voluntary SA top-up

- $500/month = $6,000/year into SA

- At 4% compounding over 25 years (40 to 65): ~$256,000 in SA by 55

- RA at 55: significant balance swept from SA (up to FRS of $220,400)

- CPF LIFE monthly payout: ~$1,700–$1,900/month from age 65

The difference between $0/month and $500/month voluntary contribution can be the difference between a comfortable CPF LIFE payout and nothing at all.

Model Uncle Lim's numbers → cpfcalculatorsg.com/calculator.html

What Counts as Net Trade Income?

NTI is your self-employment income after allowable business expenses — but it is not the same as your taxable income after personal deductions.

Allowable deductions (reduce NTI):

- Staff costs, office rent, equipment depreciation

- Professional fees (accounting, legal)

- Business-related travel

- Software subscriptions, tools, supplies

Not deductible against NTI:

- Personal income tax reliefs (CPF relief, NSman relief, parent relief)

- These come later in the income tax calculation, not at the NTI stage

Your NTI is the figure IRAS uses to calculate your MediSave obligation and pass to CPF Board.

Mixed Employment/Self-Employment Income

Some people are employed part-time or on contract while also doing freelance work.

If you have both employment income and self-employment income:

- CPF contributions (employee + employer) are made normally on the employment income

- MediSave contributions are assessed on your NTI from self-employment separately

- The two are calculated independently

However: if you've already hit the Annual CPF Contribution Limit ($37,740 for 2026) through your employment, your MediSave obligation from self-employment may be reduced or waived. CPF Board calculates this automatically when you file taxes.

Do I Need to Register with CPF Board as Self-Employed?

In most cases, no separate registration is needed. If you're a Singapore Citizen or PR doing self-employed work, IRAS and CPF Board share information automatically when you declare NTI in your income tax return.

The process:

1. File your income tax return via myTax Portal, declaring your NTI

2. IRAS passes the NTI figure to CPF Board

3. CPF Board issues your MediSave contribution notice (typically June/July)

4. You pay through the CPF portal or GIRO

No separate step required. Just make sure you're accurately declaring your NTI.

Voluntary Contributions: How to Set Them Up

Making voluntary CPF contributions is straightforward:

- Log in to my.cpf.gov.sg with Singpass

- Go to My Requests → Building Up My / My Recipient's CPF Savings

- Choose Cash Top-Up if you want the RSTU tax relief (top up to SA or RA)

- Or choose Voluntary Contribution to contribute to your CPF accounts in the standard allocation proportions

- Set up a monthly GIRO if you want automated contributions

For cash top-ups specifically targeting tax relief (RSTU scheme), use the Top-Up to SA/RA option. This is distinct from the general voluntary contribution — only RSTU top-ups generate the tax deduction.

See your numbers before committing → cpfcalculatorsg.com/calculator.html

The Tax Relief Math: Why $8,000/Year Matters

At Uncle Lim's income level ($80,000 NTI), his marginal tax rate is approximately 11.5%.

If he tops up $8,000 to SA this year:

- Tax savings: $8,000 × 11.5% = $920 cash back

- SA balance increase: $8,000 earning 4% = $320/year interest (first year)

- Net cost after tax relief: $8,000 - $920 = $7,080

For $7,080 out of pocket, Uncle Lim gets:

- $8,000 in SA earning 4% guaranteed

- $320/year compounding interest

- Stronger CPF LIFE foundation

Effective yield: well above 4% when tax savings are factored in. This is one of the most stable, government-guaranteed returns available in Singapore.

Planning for Retirement as a Freelancer

If you're freelancing long-term, here's a sustainable approach:

1. Budget for mandatory MediSave from Day 1

- Set aside 10% of monthly revenue in a separate account

- Pay the annual assessment without stress

2. Start voluntary SA top-ups early

- Even $300–$500/month compounds significantly over 20+ years

- Claim the $8,000/year RSTU tax relief every year

3. Don't neglect housing

- If you plan to buy HDB/condo, keep some voluntary contributions going to OA

- OA is needed for downpayments and mortgage repayments

4. Check your CPF balance quarterly

- Log into my.cpf.gov.sg every 3 months

- Track your OA, SA, and MA growth

- Adjust voluntary contributions as your income changes

5. At age 50, review your FRS gap

- Check how much you need to reach the Full Retirement Sum ($220,400 for 2026)

- Increase voluntary top-ups if needed in the final 5 years before 55

Frequently Asked Questions

1. Do I need to register with CPF Board as a self-employed person?

Generally no — the process is handled through your income tax return. When you declare NTI in myTax Portal, CPF Board is notified automatically. No separate CPF registration step is needed for most self-employed Singaporeans.

2. What if I earn below $6,000 NTI this year — do I still owe MediSave contributions?

No. The MediSave contribution threshold is $6,001 NTI per year. Below that, no mandatory contribution applies. But you can still make voluntary top-ups if you want to build your MA/SA.

3. My MA balance is already at the Basic Healthcare Sum. Do I still owe mandatory MediSave contributions?

If your MA has reached the BHS ($75,500 in 2026), mandatory contributions cease for the year. You may still make voluntary contributions to your OA or SA.

4. Can I claim tax relief on the voluntary CPF contributions I make to my own SA?

Yes — cash top-ups to SA (before 55) or RA (after 55) qualify for the Retirement Sum Topping-Up (RSTU) tax relief, capped at $8,000/year. Make sure you use the "Cash Top-Up" function in the CPF portal (not general voluntary contribution) to ensure IRAS recognizes it for tax relief.

5. What if I have both employment income and self-employment income?

You pay CPF normally on your employment income. Your self-employment NTI is assessed separately for MediSave. However, if you've already hit the Annual CPF Contribution Limit through employment, your self-employment MediSave may be reduced or waived.

6. Can I use my voluntary CPF contributions for housing?

Yes — voluntary contributions to OA can be used for HDB/private property downpayments and mortgage repayments, subject to the same rules as mandatory OA. Voluntary SA contributions cannot be used for housing.

7. What happens if I don't pay my mandatory MediSave contribution?

CPF Board will pursue collection. Failure to pay is a compliance issue and can result in penalties and legal action. This is a mandatory obligation, not optional.

8. I'm self-employed and planning to retire at 55. Will I get CPF LIFE?

CPF LIFE eligibility depends on having a minimum RA balance at age 65. If you only made mandatory MediSave contributions (which go to MA, not SA/RA), your RA at 55 will be minimal or zero — resulting in minimal or no CPF LIFE payouts. Voluntary SA/RA top-ups are essential for self-employed retirement planning.

9. Can I make lump-sum voluntary contributions once a year instead of monthly?

Yes. You can contribute to CPF whenever you want — monthly, quarterly, or as a lump sum. The $8,000/year RSTU tax relief cap is annual, so you can make one $8,000 top-up in December if that suits your cashflow.

10. Does the MediSave contribution count toward the $8,000 RSTU tax relief?

No. Mandatory MediSave contributions do not generate tax relief — they're an obligation, not a voluntary top-up. Only voluntary cash top-ups to SA/RA/MA above the mandatory amount qualify for RSTU relief.

Your Self-Employed CPF Checklist

- [ ] Set aside 10% of monthly revenue for annual MediSave obligation

- [ ] Declare NTI accurately in your income tax return (IRAS myTax Portal)

- [ ] Pay MediSave contribution notice when received (typically June/July)

- [ ] Start voluntary SA top-ups — even $300/month makes a difference

- [ ] Claim $8,000/year RSTU tax relief on voluntary SA/RA top-ups

- [ ] Check CPF balance quarterly at my.cpf.gov.sg

- [ ] Review retirement gap at age 50 and increase contributions if needed

Calculate your voluntary contribution impact → cpfcalculatorsg.com/calculator.html

Know a friend who just went freelance and has no idea about MediSave contributions? Share this before they get their first tax assessment surprise.

Written by the team at CPF Calculator SG. Figures based on CPF Board and IRAS policies effective January 2026. For the authoritative source, visit cpf.gov.sg. This article is for general information only and does not constitute financial advice. Next review: January 2027.