Key Takeaways

- Top up $8,000 to your SA before December 31 and save $1,200–$2,800 in income tax this year

- Year-end bonuses are subject to CPF under the Annual Wage Ceiling of $102,000 — automatic contributions apply, but voluntary cash top-ups are a separate powerful opportunity

- Voluntary cash top-ups to SA/RA qualify for income tax relief of up to $8,000/year for yourself and $8,000/year for family members under the RSTU Scheme

- The top-up must be received by CPF Board by 31 December — online transfers take 1–3 business days; safe deadline is December 24

- If your SA balance is approaching the Full Retirement Sum of $220,400, check your balance first — top-ups via RSTU stop at FRS

⏰ Do This Before December 31

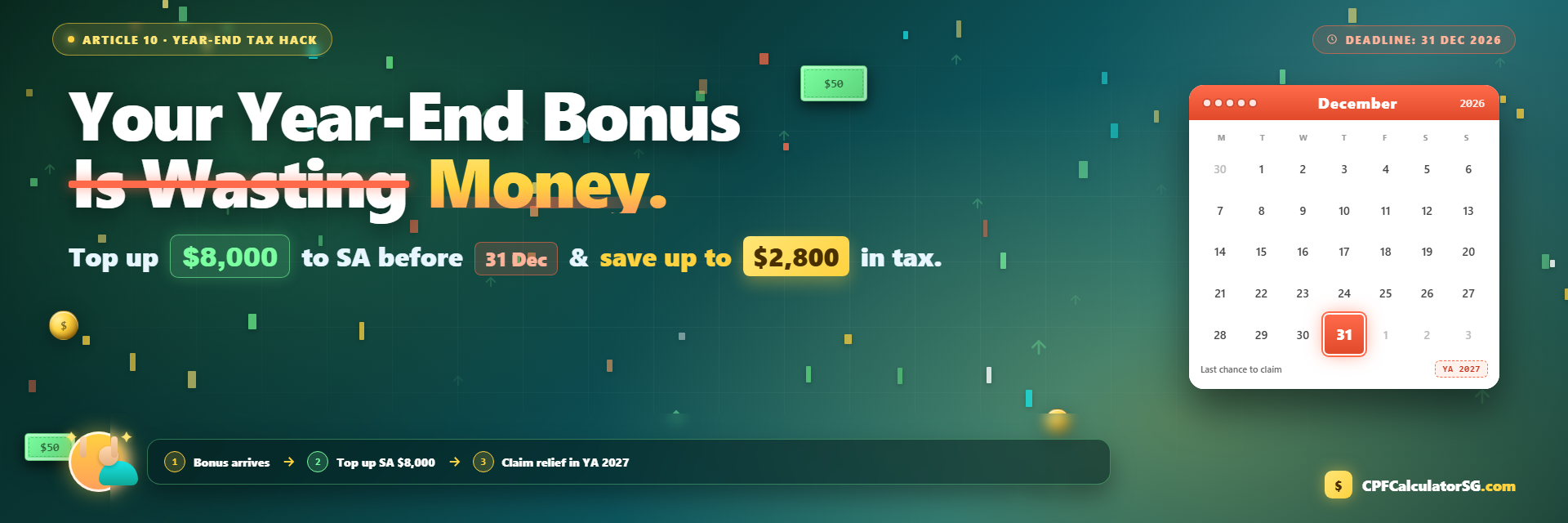

Top up $8,000 to your SA (or RA if over 55) before December 31 to reduce your chargeable income by $8,000. At a 15% marginal rate, that is $1,200 in tax saved. At 22%, it is $1,760. The money earns 4% p.a. guaranteed from day one.

Online CPF top-ups take 1–3 business days. Safe deadline: December 24. Do not leave this to the final days of December.

The Tax Saving: A Concrete Worked Example

Priya is 38, earns $90,000 a year, and receives a year-end bonus of $15,000. Her marginal income tax rate is approximately 15%.

Mandatory CPF on Bonus

- Ordinary wages: $7,500 × 12 = $90,000

- AW ceiling: $102,000

- CPF applies on bonus up to: $102,000 – $90,000 = $12,000

- Employee CPF on bonus: 20% × $12,000 = $2,400

- Remaining bonus in hand after mandatory CPF: $15,000 – $2,400 = $12,600

Voluntary SA Top-Up Decision

Priya uses $8,000 of her remaining bonus to make a voluntary SA top-up before December 31.

| Without SA Top-Up | With $8,000 SA Top-Up | |

|---|---|---|

| Chargeable income | $90,000 | $82,000 |

| Income tax (approx.) | ~$5,650 | ~$4,450 |

| Tax saving | — | ~$1,200 |

| Cash used for SA | $0 | $8,000 |

| Effective cost of $8,000 SA top-up | — | $6,800 |

Priya's $8,000 lands in SA and immediately earns 4% p.a. in guaranteed interest. The effective cost — after her tax saving — is $6,800, not $8,000. She starts with an 18% gain on her cash before any interest accrues.

If Priya also tops up $5,000 to her mother's RA, she claims an additional $5,000 in family top-up tax relief, saving another $750 in tax. Combined tax saving from $13,000 in total top-ups: ~$1,950.

How Bonuses Work in the CPF System

Your bonus is classified as an Additional Wage (AW) by CPF Board. The Annual Wage Ceiling is $102,000 for CPF contribution purposes.

The formula: mandatory CPF contributions apply to additional wages up to $102,000 minus your Ordinary Wages received that year. Your payroll system handles this calculation automatically. The voluntary top-up is entirely separate.

Higher Earners Save Even More

| Marginal Tax Rate | Tax Saved on $8,000 Top-Up |

|---|---|

| 7% (income ~$50,000–$70,000) | ~$560 |

| 11.5% (income ~$70,000–$80,000) | ~$920 |

| 15% (income ~$80,000–$120,000) | ~$1,200 |

| 18% (income ~$120,000–$160,000) | ~$1,440 |

| 19% (income ~$160,000–$200,000) | ~$1,520 |

| 22% (income ~$200,000–$320,000) | ~$1,760 |

Rates are indicative based on IRAS progressive income tax brackets.

At 22%, the $8,000 top-up delivers $1,760 in tax savings on a $6,240 net cost — a 28% immediate return before a single day of 4% interest accrues.

What If You Are Already Close to the FRS?

If your SA balance is approaching the Full Retirement Sum of $220,400, there is a limit on how much more you can top up under the RSTU Scheme. Check your balance at my.cpf.gov.sg before initiating a top-up. If you are within $2,000 of FRS, a full $8,000 top-up may be partially rejected.

If you have already met FRS and want to top up further toward the Enhanced Retirement Sum ($440,800), you can do so — but the RSTU tax relief mechanism applies only up to FRS.

Topping Up Your Spouse's Account

Year-end is a natural time to think about your household's total CPF position. If your spouse has a lower income or a gap in their SA balance, you can make a cash top-up to their SA or RA and claim the family tax relief (up to $8,000 combined for all family members, separate from your self-top-up relief).

A total of $16,000 in RSTU relief is possible in a single year ($8,000 self + $8,000 family). See CPF for Couples for the full worked example.

Common Mistakes People Make

- Missing the December 31 deadline. The top-up must be received by CPF Board, not just initiated, by December 31. Safe deadline: December 24.

- Confusing the tax relief with the top-up limit. Only the first $8,000 gets tax relief. The excess still earns 4% in SA but gives no additional income tax benefit.

- Not checking the SA ceiling before topping up. If your SA is within $1,000 of the FRS ($220,400), a full $8,000 top-up may be partially rejected.

- Forgetting about parents. The $8,000 family top-up relief is separate from your self-top-up relief.

How to Make the Top-Up (Step-by-Step)

- Log into my.cpf.gov.sg using Singpass

- Navigate to "Top up my CPF" under the Retirement section

- Select "Top up using cash" under the Retirement Sum Topping-Up Scheme

- Choose the recipient (self, spouse, parents, etc.)

- Enter the amount (up to $8,000 for self-top-up tax relief)

- Complete payment via PayNow, internet banking, or AXS

CPF Board automatically reports top-ups to IRAS, and the relief should appear pre-filled in your tax return.

Check your current SA balance against FRS and see exactly how much room you have to top up.

Check Your SA Balance →Frequently Asked Questions

Can I use my bonus for an OA-to-SA transfer instead of a cash top-up?

Yes — but it is a different mechanism and has no tax relief attached. An OA-to-SA transfer moves money already inside CPF from one account to another. The cash top-up under RSTU is what delivers the income tax saving. You can do both in the same year.

What if I miss the December 31 deadline?

The top-up counts for the following tax year. You have not lost the opportunity; you have delayed it by 12 months.

Does the SA top-up count toward my FRS target?

Yes. Any voluntary cash top-up to your SA under RSTU increases your SA balance, which contributes toward your FRS target of $220,400 at age 55.

Can I contribute to both CPF RSTU and SRS in the same year?

Yes. They fall under different tax relief categories. CPF RSTU top-ups give up to $8,000 relief. SRS contributions give up to $15,300 (Singapore Citizens and PRs). Both can be claimed in the same tax year. Note that total personal income tax reliefs are capped at $80,000 per year across all categories.

What happens to the $8,000 in SA if I need the money urgently?

Once in SA, voluntary RSTU top-ups cannot be withdrawn before age 55. Only make the top-up if you genuinely will not need that cash before retirement.

Written by the team at CPF Calculator SG. Reviewed against CPF Board policies effective January 2026. For the authoritative source, visit cpf.gov.sg. This article is for general information only and does not constitute financial advice.